The Lowes UK Defined Strategy Fund (the “Fund”), launched in December 2018. Since inception the initial portfolio has been constructed, consisting of a mixture of auto-callable notes and ‘Over-The-Counter’ (“OTC”) contracts backed by gilts. Although the Fund can invest up to 20% of its assets in investments linked to overseas indices, all the contracts in the current portfolio (as of 15/05/2023) are linked to either the FTSE 100 Index or the FTSE Custom 100 Synthetic 3.5% Fixed Dividend Index (FTSE CSDI).

The Fund contains a portfolio of auto-callable structured notes and over the counter (OTC) contracts, each of which have different maturity parameters with defined outcomes, that vary as market conditions vary. For the purposes of this article each of these structured notes and OTC contracts may be referred to as a ‘strategy’. As of 16/05/2023, there are a total of 20 different strategies within the portfolio, ranging from those that require the Index to be at or above the Initial Index Level to mature with a gain, to ones where the Index can drop up to 20% at maturity and still produce a gain. This, combined with the staggering of the investments, means that the Fund contains strategies which will return a gain on their final potential maturity date at a range of different Index values, subject to the continuing solvency of the counterparty issuing the strategy in the case of the structured notes. Further details upon each of these strategies can be viewed by anyone eligible to invest in the Fund at UKDSF.com/Portfolio.

Lowes Investment Management Ltd, (the Investment Manager), have diversified the counterparty exposure in accordance with UCITS regulations, limiting counterparty credit exposure by spreading the auto-callable notes across three separate investment grade banks, and all the OTC contracts are backed by a portfolio of short-dated gilts.

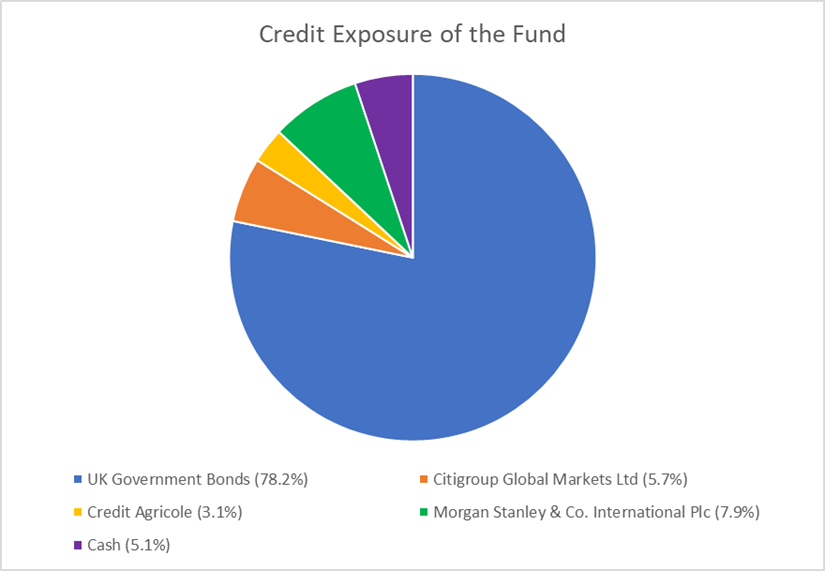

The below chart displays the credit exposure of the Fund, as of the 15th May 2023.

Source: UKDSF.com/Portfolio.

As of the 15th May 2023, the Fund has 5.1% in cash, and 78.2% in gilts and gilt backed contracts. The returns offered by the strategies in return for assuming credit risk from banks tends to be higher than strategies utilising gilts and OTC contracts, due to the credit risk premium assumed by the investor, assuming other factors such as volatility, and interest rates remain equal.

The more obvious risk contained within the Fund is market risk. This is where an investor exposes their capital to the fluctuations in the movements of the underlying assets; namely the FTSE 100 Index and the FTSE CSDI for this Fund. There are several ways in which investors can assess market risk. In the case of the Lowes UK Defined Strategy Fund, we measure the sensitivity of change in the Fund’s value relative to the underlying index through a measure called Delta. A Delta of 1 would indicate that the Fund should move in line with the underlying, whilst a Delta of 0.5 would indicate that the Fund should rise or fall by 50% of the movement in the underlying. Given that the Fund diversifies across varying strike dates, maturity parameters, and strike levels, we would expect the Fund’s Delta to be less than that of the underlying assets in the medium-to-long term, assuming all but the most extreme market conditions.

The Investment Manager has chosen a variety of strategies with varying Deltas and levels of credit risk to manage the overall risk of the portfolio. By diversifying the credit risk of the portfolio, and in the case of the OTC contracts removing it altogether, we reduce the potential for the Fund to lose value as a result of counterparty default. For information in relation to Fund risks please reference the Fund Supplement – access information can be found at the end of this article.

Here are a few examples:

Fund Autocall Strategy 13 – A strategy that requires the underlying to be at or above a reducing maturity trigger level

An eight-year strategy that can mature from year one onwards providing the FTSE 100 Index is at or above a reducing maturity trigger level, starting from 105% of the Initial Index Level in years one and two, reducing to 100% in years three and four, 95% in year five, 90% in year six, 85% in year seven and finally 80% in year eight. This strategy contains a capital protection barrier of 60% that will only be observed at the end of the eight-year term, providing the strategy does not mature early. Potential Return: 7.76% for each year the strategy is held. Credit Exposure: Citigroup Global Markets Ltd

Fund Autocall Strategy 53 – A strategy that requires the underlying to be at or above a reducing maturity trigger level

An eight-year strategy that can mature from year one onwards providing the FTSE CSDI is at or above a reducing maturity trigger level, starting from 100% of the Initial Index Level in years one and two, reducing to 95% in years three, four and five, and finally to 90% in years six, seven and eight. This strategy contains a capital protection barrier of 65% that will only be observed at the end of the eight-year term, providing the strategy does not mature early. Potential Return: 9.37% for each year the strategy is held. Credit Exposure: Morgan Stanley & Co. International Plc

Fund Autocall Strategy 54 – A strategy that requires no growth in the underlying

An eight-year gilt collateralized strategy that can mature from year one onwards providing the FTSE CSDI is at or above 100% of the Initial Index Level. This strategy contains a capital protection barrier of 65% that will only be observed at the end of the eight-year term, providing the strategy does not mature early. Potential Return: 10.16% for each year the strategy is held. Credit Exposure: UK Government Bonds

The portfolio will continue to evolve as new money comes in and existing strategies mature. Depending on pricing, market levels and outlook at that time new strategies may be added, or existing ones may be increased. Before being added to the Fund, all strategies are subject to rigorous back testing, whilst considering the current position of the portfolio and behaviour of the underlying asset (for example, the FTSE 100 Index or the FTSE CSDI). Strategies are not selected solely upon their own merits, but in the context of their contribution to the wider portfolio.

The source for all information in this article can be found at UKDSF.com/Portfolio or is otherwise sourced by Lowes Investment Management.

If you would like to know more about the Lowes UK Defined Strategy Fund, please visit the Fund website (UKDSF.com) or call Lowes Investment Management on 0191 281 88 11.

Further Information:

This article is for information purposes only and should not be construed as advice. We strongly suggest you seek independent financial advice prior to taking any course of action.

The value of this investment can fall as well as rise and investors may get back less than they originally invested. Past performance is not necessarily a guide to future performance.

The Fund is suitable for investors who are seeking capital growth over a medium to long term horizon but who are willing to tolerate medium to high risks due to the potentially volatile nature of the investments.

The Lowes UK Defined Strategy Fund is a sub-fund of the Skyline Umbrella Fund ICAV and is regulated by the Central Bank of Ireland. The KIID, Prospectus, and Supplement can be accessed by visiting UKDSF.com/Literature and are only available in English.

Lowes Investment Management Ltd, Fernwood House, Clayton Road, Newcastle upon Tyne, NE2 1TL. Authorised and regulated by the Financial Conduct Authority.